Text adapted from: "Disability and insurance claims in primary care," in Psychiatry in primary care by Ash Bender (CAMH, 2019).

Key definitions

Impairment: problems with body function or structure, such as a significant deviation or loss (WHO, 2001).

Disability: health-related restriction or lack of ability to perform an activity within a range considered normal (WHO, 1980). Within a claims context, disability is defined by the specific terms of an insurance policy.

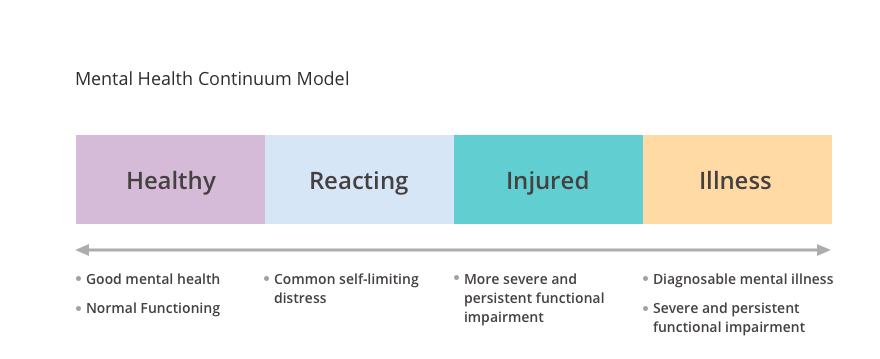

As captured by the Mental Health Continuum Model (see below), adapted from the United States Marine Corps, impairment can be dynamic, and may be persistent for some people, but not for others. As a rule, total disability occurs only when demands cannot be met or modified sufficiently to accommodate the mental health impairment.

Documentation: All insurers, including government-sponsored workers’ compensation programs, require adequate medical documentation in order to support a mental health disability claim. Although documentation can be onerous, failure to complete documents properly will result in significant distress and financial burden to your patient. More recently, physicians have been found liable for failing to provide documentation in a timely and complete manner. Completing forms in a timely and legible way ensures that your patients receive benefits to which they are entitled.

Physicians are not required to provide medical information directly to employers and should only do so after they obtain the patient’s consent (Demeter & Andersson, 2003). Follow these tips to ensure your documentation is complete:

- Document when symptoms and impairment first appeared because disability payments may be made retroactively

- List all supporting symptoms for the most responsible diagnosis

- Use DSM diagnostic criteria whenever possible

- Provide an evidence-based treatment plan with return to work as a goal

- Recommend any further investigations or treatment you cannot provide

- Clearly document how the patient is impaired or limited in performing work duties

- Recommend work restrictions to limit risk of aggravation of the patient’s condition

- Suggest accommodation of specific duties, but not specific jobs

- Recommend extended time off work as a last resort

Compensation: Most occupation-related medical services and forms are not covered under provincial and territorial insurance plans and require separate billing. In such cases, the physician should submit an invoice with a request for reasonable compensation. Most government-based requests have fixed fees that are clearly identified on the forms.

Insurance companies or lawyers may not provide information related to fees, and it is suggested that a fee be agreed upon before proceeding. Rates for these services are typically higher than government-funded remuneration. Regulatory bodies and medical associations can provide guidelines for billing (e.g., Ontario Medical Association, 2017).

Examples of services to third-party providers that would be billed for include:

- Document preparation and file transfer

- Telephone calls or consultations with insurance companies

- insurance certificates and reports

- medical examinations or procedures for licensing or insurance

- Canada Pension Plan and Workers’ Compensation reports

In Disability and Insurance Claims in Primary Care

- Overview

- Key Definitions

- Documentation and claims

- Documenting a Diagnosis

- Facilitating the patient's return to work

- Resources and References